A Practical Guide: how to read income statement for beginners

Learn how to read income statement with this practical guide. We break down revenue, margins, and ratios for investors and finance professionals.

Reading an income statement isn't about memorizing formulas; it's about following a story from top to bottom. You start with the headline—total revenue—then subtract the direct costs to see the initial plot twist, gross profit. From there, you deduct all the other operational costs to get operating income, and finally, after dealing with interest and taxes, you arrive at the story's conclusion: net income, the famous bottom line.

Decoding the Profit and Loss Story

An income statement, often called a Profit and Loss (P&L) statement, tells you exactly how a company performed over a specific period, whether that's a quarter or a full year. It’s not a snapshot like a balance sheet. Think of it more like a movie that shows you everything that happened—all the sales made and all the bills paid—from the beginning of the period to the end.

Getting comfortable with this document is essential for understanding a company's real financial health. It’s a cornerstone of fundamental analysis and is absolutely critical knowledge if you're interviewing for roles in finance, consulting, or any position where you need to prove your business savvy.

To make this practical, let's walk through the key components.

The Top Line: Revenue

Everything starts at the top with Revenue, sometimes called Sales. This number is the total amount of money a company brought in from its primary business activities before a single expense is taken out. It’s the purest indicator of a company's ability to sell its products or services.

For a local coffee shop, this would be the sum of every latte, muffin, and bag of beans sold that month. It’s the raw number you see at the register before you start paying for rent, beans, or your baristas.

Cost of Goods Sold and Gross Profit

Right below revenue, you'll find the Cost of Goods Sold (COGS). These are the direct costs of producing what the company sells. For our coffee shop, this is the money spent on coffee beans, milk, sugar, and paper cups. It does not include the barista's salary or the shop’s rent—we'll get to those in a bit.

Subtract COGS from Revenue, and you get Gross Profit. This is your first crucial checkpoint.

Gross Profit = Revenue - Cost of Goods Sold

This figure tells you how efficiently a company makes its product. A healthy gross profit means there's a good chunk of money left over to cover all the other costs of running the business.

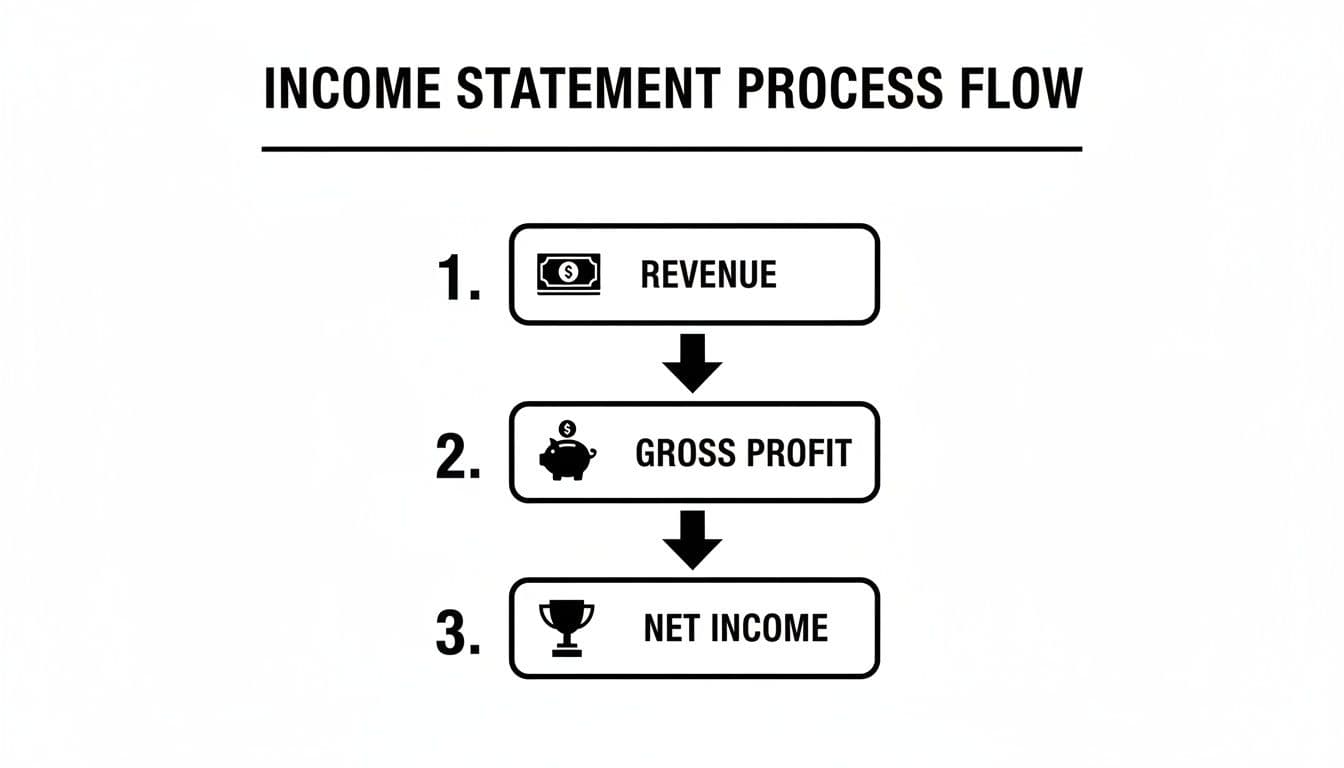

The flow is simple, as this chart illustrates.

This visual breaks down how profit is calculated at each stage by systematically subtracting different layers of costs from that initial revenue figure.

Here’s a quick-reference table to keep these core concepts straight.

Key Components of an Income Statement

| Line Item | What It Measures | Simple Analogy |

|---|---|---|

| Revenue | Total sales from goods or services. | The price tag on everything you sold. |

| COGS | Direct costs of creating those goods or services. | The cost of your ingredients (flour, sugar). |

| Gross Profit | Profit left after covering direct production costs. | What's left after paying for ingredients. |

| OPEX | Indirect costs of running the business. | The cost of rent, salaries, and marketing. |

| Operating Income | Profit from core business operations. | What's left after paying for ingredients and running the store. |

| Net Income | The final "bottom line" profit after all expenses. | The actual cash you can take home. |

This table provides a simple, at-a-glance way to remember what each line item in the profitability story really means.

Operating Expenses and Operating Income

Next up are the Operating Expenses (OPEX). These are all the costs needed to keep the lights on that aren't directly part of the product itself. It’s a pretty broad category that typically includes:

- Selling, General & Administrative (SG&A): This is a big one. It covers salaries for your marketing team and executives, advertising costs, rent, and utility bills.

- Research & Development (R&D): For tech and pharma companies, this is a huge expense related to creating new products.

- Depreciation & Amortization: These are non-cash expenses that account for the gradual loss in value of assets like machinery or buildings over time.

When you subtract all of these operating expenses from the Gross Profit, you get Operating Income. You'll often see this called EBIT, which stands for Earnings Before Interest and Taxes. This metric is a fantastic indicator of a company's core profitability and how well its management team is running the day-to-day business.

The Bottom Line: Net Income

We're almost at the end. After calculating operating income, we have to account for a few final items, mainly interest payments on debt and corporate taxes.

Once you subtract those, you finally arrive at the Net Income—the "bottom line." This is the profit that's truly left over for the company and its shareholders. If this number is positive, the company made money. If it's negative, it took a loss. Learning how to properly interpret these figures is a key skill, and you can learn more about it in our guide on https://soreno.ai/articles/how-to-analyze-financial-statements.

While most news headlines fixate on this final number, the real story—and the most valuable insights—are found by understanding the journey from the top line all the way down.

Moving Beyond Raw Numbers to Margin Analysis

Just reading the line items on an income statement is only half the battle. The real insight—the kind that separates a novice from an expert—comes from turning those absolute dollar amounts into percentages, or margins. This is where the numbers start telling a story about a company's efficiency, pricing power, and overall health.

Think of it this way: margin analysis is how you move from "what happened" to "how well did it happen?" Context is everything. A $1 million net income sounds great on its own, but it tells a very different story if it came from $100 million in revenue versus $2 million.

Percentages put everything on a level playing field. They allow you to benchmark a company's performance against its own history, its closest competitors, or the industry at large. Learning to see an income statement through the lens of margins is the key to unlocking what's really going on under the hood.

Unpacking Gross Profit Margin

The first, and perhaps most fundamental, margin you'll calculate is the Gross Profit Margin. This tells you exactly how much profit a company squeezes from each dollar of revenue before any corporate overhead is factored in. It’s all about the profitability of the product or service itself.

The formula is dead simple:

Gross Profit Margin = (Gross Profit / Total Revenue) x 100

A healthy gross margin is a sign of strong pricing power or a serious cost advantage. For example, a software-as-a-service (SaaS) company might boast a gross margin of 85% because the cost to deliver its product to one more customer is virtually zero. A grocery store, on the other hand, might operate on a 20% gross margin because it has to buy every single item it sells.

This one number gives you incredible insight into the core business model right from the start.

Gauging Operational Efficiency with Operating Profit Margin

Next up is the Operating Profit Margin. This metric digs deeper, revealing what percentage of revenue is left after all the core costs of doing business—both COGS and operating expenses like marketing, salaries, and rent—are paid.

Here’s the calculation:

Operating Profit Margin = (Operating Income / Total Revenue) x 100

This margin is my go-to indicator for judging management's efficiency. A company with a strong and growing operating margin is proving it can keep its day-to-day costs in check while still fueling sales.

Here's a classic red flag: if you spot a company with a beautiful gross margin but a weak operating margin, it could mean their administrative or marketing spending is out of control. It tells you how profitable the main business is, stripping away the noise from financing decisions or tax strategies. To really dig in, analysts will often look at specific expenses within this category, which is where a solid grasp of what is unit economics becomes incredibly powerful.

The Final Verdict: Net Profit Margin

Finally, we arrive at the Net Profit Margin, the ultimate measure of profitability. It's the proverbial "bottom line," showing the percentage of revenue that trickles all the way down into pure profit after every single expense—including interest and taxes—is accounted for.

It's calculated as:

Net Profit Margin = (Net Income / Total Revenue) x 100

If a company has a 15% net profit margin, it means it gets to keep $0.15 of every dollar it earns. While this is a critical metric, you have to be careful. It can be easily distorted by one-off events. A big asset sale or a change in tax laws could temporarily spike or depress the net margin, masking the true health of the core business.

That’s precisely why you need to look at all three margins together. They paint a complete picture:

- Gross Margin: How profitable is the product itself?

- Operating Margin: How efficient are the core business operations?

- Net Margin: After all is said and done, how much cash is left for shareholders?

Why EBIT and EBITDA Matter So Much

When you're comparing companies, especially across industries or countries, Net Income can be a flawed yardstick. Differences in debt levels (which affects interest expense) and tax rates can make an apples-to-apples comparison impossible. This is where EBIT and EBITDA become your best friends.

- EBIT (Earnings Before Interest and Taxes): This is just another name for Operating Income. It lets you compare the core operational profitability of two companies without the distortion of their capital structure or tax situations.

- EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization): This metric goes even further by adding back non-cash charges like depreciation. It's often used as a quick-and-dirty proxy for a company's operating cash flow.

EBITDA is particularly useful when analyzing capital-intensive businesses, like manufacturing or telecom, where massive depreciation charges can make a company look less profitable than it actually is from a cash-generating perspective. It helps you see the underlying operational engine more clearly. Mastering these margins is a non-negotiable skill for anyone serious about financial analysis.

Uncovering the Story with Trend and Comparative Analysis

An income statement from a single quarter is just a snapshot. It’s useful, but the real story—the narrative of a company's health and trajectory—only comes alive when you look at the bigger picture. This means comparing performance over time and against competitors.

That's where trend and comparative analysis come in. These are the tools that let you move beyond static numbers and start asking the important questions. Is revenue growth picking up steam or starting to fizzle out? Are profit margins getting stronger, or are they being squeezed by rising costs? This is how you spot the subtle patterns that tell you where a business is really headed.

Spotting Patterns with Trend Analysis

Trend analysis, also known as horizontal analysis, is simply the practice of lining up several income statements—from the last few quarters or years—and comparing each line item. The most common approach here is a year-over-year (YoY) comparison, which is great for seeing real growth and smoothing out any seasonal weirdness.

Let’s say you’re looking at a retail company that grew its revenue by 10% last year. On the surface, that sounds pretty good. But what if it grew 20% two years ago and 15% the year before that? Suddenly, that 10% figure looks less like growth and more like a slowdown—a potential red flag that warrants a closer look.

Here’s what I always look for when doing a trend analysis:

- Revenue Growth: Is it accelerating, slowing down, or holding steady? Any sudden jumps or drops need an explanation.

- Cost Creep: This is a classic trap. Are the costs of goods sold or operating expenses growing faster than revenue? If so, profitability is shrinking, which could point to major inefficiencies.

- Margin Stability: Are the company’s gross and operating margins expanding, contracting, or holding firm? Shrinking margins can be a clear sign of intense competition or rising supply costs.

Tracking these metrics over time isn't just about crunching numbers. It's a way to grade management's performance. Consistent, positive trends tell you the leadership team is executing its strategy effectively. Erratic or negative trends raise serious questions about the long-term viability of their business model.

Leveling the Playing Field with Common-Size Analysis

How can you possibly compare the operational efficiency of a behemoth like Amazon with a tiny e-commerce startup? Their dollar figures are in completely different universes, so a direct comparison is useless. The answer is common-size analysis.

This technique is a favorite in finance interviews for a reason—it’s powerful. It works by converting every single line item on the income statement into a percentage of total revenue. By doing this, you instantly remove the distortion of size and get a standardized P&L that allows for a true apples-to-apples comparison.

Creating a Common-Size Income Statement

The process is straightforward: just divide each line item by total revenue for that period, then multiply by 100 to get a percentage.

- Revenue is always your baseline, so it’s 100%.

- Cost of Goods Sold might be 40% of revenue.

- That means Gross Profit is 60% (which is your Gross Margin).

- Marketing expenses might be 15% of revenue, R&D could be 10%, and so on down the line.

Now, you can put that startup’s common-size statement next to Amazon’s. If the startup boasts a gross margin of 70% while Amazon’s is 45%, you've just uncovered a critical insight. The smaller company might have a much more profitable core product or a smarter pricing strategy, even if its actual dollar profit is a drop in the bucket compared to Amazon's.

Learning to think in these relative terms is a core skill, especially for anyone figuring out how to build financial models for valuation or strategic planning. This context is everything—it reveals a company's competitive strengths and weaknesses in a way that raw numbers never could.

Putting It All Together: A Real-World Walkthrough

Theory is great, but let's get our hands dirty. Understanding the individual lines on an income statement is one thing; weaving them together to tell a story about a business is the real skill. This is exactly what you’ll be asked to do in any finance or consulting role.

Let’s analyze a fictional software company, "InnovateTech." We’ve got their income statements for the past two years. The goal isn't just to read the numbers, but to diagnose the company's health, question its strategy, and form a sharp opinion on its performance.

The Initial Data Dump

First, we lay out the raw numbers. This is always the starting point—just a simple side-by-side comparison to get a feel for the absolute figures.

| Metric | Year 1 ($M) | Year 2 ($M) |

|---|---|---|

| Revenue | $500 | $600 |

| Cost of Goods Sold (COGS) | $100 | $132 |

| Gross Profit | $400 | $468 |

| Operating Expenses | $250 | $330 |

| Operating Income (EBIT) | $150 | $138 |

| Interest & Taxes | $45 | $41 |

| Net Income | $105 | $97 |

Right off the bat, you see a mixed bag. Revenue is up, which is great. But then your eyes drift down, and you see that Operating Income and Net Income actually fell. This is a classic red flag—top-line growth that might be hiding some serious underlying problems. Now, we need to dig in.

Running the Numbers: Trend and Common-Size Analysis

To figure out what’s really going on, we’ll run two of the most powerful analyses in our toolkit: Year-over-Year (YoY) growth and a common-size analysis. The common-size view, which shows each line as a percentage of revenue, is fantastic for understanding a company’s cost structure and how it's changing.

Let's expand our table with these new calculations.

Sample Company Income Statement Analysis

Here’s the side-by-side comparison for InnovateTech, now including our key ratio calculations. This table transforms the raw data into actionable insights, showing us not just what changed, but by how much and in what proportion.

| Metric | Year 1 ($M) | Year 2 ($M) | YoY Growth (%) | Common-Size % (Year 2) |

|---|---|---|---|---|

| Revenue | $500 | $600 | +20.0% | 100.0% |

| COGS | $100 | $132 | +32.0% | 22.0% |

| Gross Profit | $400 | $468 | +17.0% | 78.0% |

| Operating Expenses | $250 | $330 | +32.0% | 55.0% |

| Operating Income | $150 | $138 | -8.0% | 23.0% |

| Net Income | $105 | $97 | -7.6% | 16.2% |

By adding growth rates and percentages, the story sharpens dramatically. We can now pinpoint exactly where the operational leaks are and start asking the tough questions.

The new columns tell a much clearer story. The YoY growth figures are practically screaming at us: COGS (+32%) and Operating Expenses (+32%) grew way faster than Revenue (+20%). That’s a surefire recipe for shrinking profits.

Key Takeaway: Revenue growth is just vanity if it doesn't translate to profit. The real skill is spotting when costs are running hotter than sales—that’s where value is being destroyed.

Interpreting the Results and Asking "Why?"

The numbers tell us what happened. Our job is to figure out why. This is where financial analysis connects directly to business strategy.

-

Gross Margin Squeeze: InnovateTech’s COGS went from 20% of revenue in Year 1 ($100M / $500M) to 22% in Year 2. A two-point drop in gross margin is significant. Why did this happen? Were they forced to lower prices to win deals? Did their input costs, like server hosting or third-party software licenses, shoot up?

-

Bloated Operating Expenses: This is the big one. OPEX jumped from 50% of revenue in Year 1 ($250M / $500M) to a whopping 55% in Year 2. That five-point increase is what really crushed their operating income. So, what’s the story? Did they go on a hiring spree for a new sales team that isn't productive yet? Did they pour money into a huge marketing campaign that fell flat?

These questions are the entire point of the exercise. A good analyst doesn't stop at the numbers; they use them to form hypotheses about the actual business operations. For global companies, operational efficiency is everything, a point often stressed in reports on wealth and economic trends. You can find more insights on these global financial dynamics in Allianz’s comprehensive analysis.

This process is your repeatable framework. Start with the raw data, calculate YoY growth and common-size percentages to see the trends, and then—most importantly—translate those numbers into sharp, strategic business questions. That’s how you turn a simple P&L into a powerful diagnostic tool.

Answering Tough Interview Questions About Income Statements

Knowing your way around a P&L is table stakes. But in a high-pressure interview, simply reciting definitions won't cut it. The real test is connecting the numbers to a business strategy and telling a clear, compelling story about what they mean.

This is where you show you can think like an analyst. Let’s break down some of the most common—and trickiest—interview prompts so you can walk in ready to prove your business acumen, not just your accounting knowledge.

Prompt 1: Walk Me Through an Income Statement

This question seems simple, but it’s a test of your communication skills and foundational understanding. The worst thing you can do is just list the line items. Instead, you need to tell the story of how a company makes money.

A strong answer flows logically from top to bottom, explaining the why behind each major section.

"Absolutely. The income statement really tells the story of a company’s profitability over a specific period.

It starts at the very top with Revenue—all the money brought in from sales. Right away, we subtract the Cost of Goods Sold (COGS), which are the direct costs tied to making the product. What’s left is Gross Profit, which gives us our first real read on how profitable the company's core business model is.

From there, we have to account for the costs of actually running the business, which fall under Operating Expenses—things like marketing spend, R&D, and salaries. Subtracting those gives us Operating Income, or EBIT. This is a crucial metric because it shows the profitability of the main business operations, separate from financing or tax strategies.

Finally, we take out non-operating items like interest payments and taxes, which brings us to the famous bottom line: Net Income. That's the actual profit left over for the shareholders."

This approach is concise, logical, and shows you grasp the narrative of profitability.

Prompt 2: What Does a High Gross Margin but Low Net Margin Suggest?

This is a diagnostic question. The interviewer wants to see if you can pinpoint where a business is "leaking" profit between making its product and what it ultimately keeps.

Your answer should show you can isolate the problem.

- Start by acknowledging the good news. "A high gross margin is a fantastic sign. It tells me the company either has strong pricing power or a very efficient production process."

- Zero in on the problem area. "But if the net margin is low, that profitability is getting wiped out before it hits the bottom line. The issue must be with high operating costs or significant non-operating expenses."

- Offer specific, educated guesses. "I'd investigate a few things. It could be bloated SG&A (Selling, General & Administrative) expenses—maybe an inefficient sales team or high corporate overhead. Another likely culprit is a heavy debt load, which would lead to high interest expense eating into profits."

This kind of response shows you can move beyond the numbers to form a hypothesis about the underlying business challenges.

Prompt 3: How Can a Profitable Company Run Out of Cash?

This is the classic question that separates those who understand accounting from those who understand business. It gets right to the heart of the difference between accrual accounting (the income statement) and cold, hard cash flow.

The key is to explain that profit isn't cash in the bank.

- Address the core concept head-on. "That's a great question that highlights the critical difference between profit and cash. An income statement can look great, but if the cash isn't coming in the door, the business is in trouble. This disconnect usually comes down to working capital and major investments."

- Give a clear example with Accounts Receivable. "For instance, a company could make a huge sale on credit. That revenue gets booked immediately, boosting net income. But if the customer takes 90 days to pay, the company has no cash from that sale to pay its own employees or suppliers. It's just an IOU, or an account receivable."

- Explain the impact of Inventory. "It could also be an inventory issue. The company might spend a ton of cash building up products, but that cash is gone. The expense doesn't hit the income statement as COGS until the product actually sells, so the P&L can look healthy while the bank account is draining."

- Bring in Capital Expenditures. "Finally, big investments like capital expenditures—buying a new factory or upgrading equipment—are huge cash drains. These don't appear on the income statement, except as a small, non-cash depreciation charge each year. A company could be profitable but spend all its cash on a new building and find itself unable to make payroll."

Answering the Tough Questions

Once you get the hang of reading an income statement, you start running into the trickier questions—the kind that pop up in technical interviews. Let's tackle a few of the most common ones to really cement your understanding.

What's the Real Difference Between EBITDA and Net Income?

Think of it this way: EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) is a snapshot of a company's raw operational muscle. It shows how profitable the core business is before you account for financing decisions, tax strategies, or non-cash expenses. It's often used as a quick-and-dirty proxy for cash flow.

Net Income, on the other hand, is the final "bottom line." It’s what’s left for shareholders after every single expense gets deducted—interest, taxes, and those non-cash charges included. So, while EBITDA shows you the engine's horsepower, Net Income tells you how much of that power actually makes it to the finish line as pure profit.

Why Would a Profitable Company Go Bankrupt?

This is a classic interview question designed to test if you understand the crucial difference between profit and cash. A company can post a healthy Net Income and still go under if it runs out of cold, hard cash to pay its bills.

How does this happen? It usually comes down to a few key culprits:

- Slow-Paying Customers: Revenue is booked when a sale is made, not when the cash comes in. If your customers are taking forever to pay their invoices (high accounts receivable), you have profits on paper but an empty bank account.

- Piling Up Inventory: A company might burn through a ton of cash to manufacture products. That cash is gone, but the expense doesn't hit the income statement as COGS until the product is actually sold. This creates a dangerous cash gap.

- Huge Debt Payments: Principal payments on loans are a massive cash drain, but they don't show up on the income statement at all (only the interest portion does). A company can be "profitable" while being bled dry by its debt obligations.

The bottom line: Profit is an accounting opinion, but cash is a fact. A business needs actual cash to pay salaries, keep the lights on, and satisfy lenders, no matter what its Net Income says.

Is It Possible for a Company to Have a Negative Gross Profit?

Yes, but it's a five-alarm fire. A negative Gross Profit means the direct cost of making the product (COGS) is higher than the price the company is selling it for.

In simple terms, they are literally losing money on every single sale before even thinking about paying for things like marketing, salaries, or rent. This isn't just a bad sign; it's a sign of a fundamentally broken business model that's completely unsustainable.

Where Can I Find a Company's Income Statement?

For any publicly traded company, these documents are readily available—it's the law. The most official source is the SEC's EDGAR database, where you can dig into their quarterly reports (Form 10-Q) and annual reports (Form 10-K).

If you're looking for a more digestible format, head over to the "Investor Relations" section of the company's own website. Financial data providers like Yahoo Finance or Bloomberg also do a great job of presenting this information cleanly. For more hands-on advice, check out another practical guide on how to read income statements.

Ready to master the case interview? Soreno provides an AI-powered platform with over 500 cases and guided drills to sharpen your analytical skills. Practice with an AI interviewer that gives you rubric-based feedback on structure, communication, and business insight. Get unlimited reps, pinpointed notes, and the confidence to land your dream consulting or finance offer. Start your 7-day free trial today at https://soreno.ai.